Those two words draws up images which likely cause

Alfred Sloan to roll over in his grave. What do I think of when I think of GM? The worst management this side of the Berlin Wall. Cars only rivaled by those made in the former Soviet Union in their ugliness and, at times, quality. Two of GM's finest are pictured above. The Buick Roadmaster wagon and the Pontiac Aztek.. Two cars of many that are a total embarrassment. The utterance of General Motors used to cause fear in every corner of the globe. A dominant empire and sign of America's technological and manufacturing might.

I actually worked for GM as an engineering co-op in college and am an avid automobile enthusiast who hopes for the day GM gets its act together. During my stint, only the best could dream of working for GM. Well, except for co-ops which explains my situation. lol. In fact, GM had their own technical college, GMI, which was one of the most prestigious engineering schools in the world and extremely difficult to get into. Today, it no longer is affiliated with GM and thus the prestige and reputation have diminished. It is now

Kettering University. At one time, its reputation was akin to MIT or Stanford as a degree from GMI held significant weight regardless of where you worked.

What happened? In a nutshell, they were insulated from competition and truly did become something akin to the monolithic car makers of the Eastern Bloc. The high volume automobile business is not something which has historically drawn alot of new competition. The engineering, plant, dealership and capital equipment costs are mind boggling. The cost of developing a single new platform can be as high as $3-4 billion dollars. General Motors, Toyota, Ford, Volkswagon, Honda and others cumulatively spend so much money in new product development that it is mind boggling. Large companies launching 10-20 new or refreshed designs a year on a global basis requires some serious cash. GM, as an example, has nearly $300 billion in debt and before the recent rise of its stock, its market capitalization was about $9 billion. You want to buy GM? No problem. You want $300 billion in debt to go with those fries? You want to enter the high volume automobile business? No problem. Got a cool fifty billion to bet on chance? The Japanese, Korean and Chinese governments did. Frankly, that is how all of the Asian automakers got started. Government cash and government protection.

GM first ceded the small car market believing they could move upscale and let the Japanese build low profit small cars. Soon, it was apparent the Japanese were using small car profits to fund designs of larger cars. So, GM decided they would modernize. Robots, robots and more robots. One of the worst CEOs in American history, Roger Smith, spent something like $60 billion modernizing GM to compete with Toyota. Instead of spending that money to modernize, GM could have bought Toyota, Honda and Nissan for that same amount of money. And, what did we get for that investment? Well, I had a buddy who worked at the GM Hamtramck plant where robots were to do everything including eat Toyota's lunch. The end result was robots welding other robots and GM ripping much of the automation out. When this didn't fail to stop the market share losses, GM decided it would get into other businesses so it bought EDS and then Hughes Aircraft. But, the market share losses didn't stop and GM found out building missiles wasn't the same as building cars. So, after spending billions of dollars to buy these companies, they were sold.

So, we've seen GM retreat from market after market as the small Japanese manufacturers used profits and superior quality to move from subcompacts to compacts to midsize to luxury to sport utility to pickups. All the while, GM's market share dropped from 60% to about 24% today. Of that 24%, how many sales are to

low margin auto rental businesses and to GM employees, supplier employees, dealership employees, family of GM workers, etc. Does GM actually sell anything to someone not affiliated with GM? If that isn't enough, GM bet its business on SUVs and full size pickups AFTER the attack of 9/11. No thought was given to hybrids, moving up small car or midsize car programs with better gas mileage or any thought that oil, at $10 a barrel would rise due to global demand or risk now baked into the terrorist dilemma. Hello, is anyone home at GM?

And, for all of this, GM executives have made billions and billions in compensation over the last thirty years while GM has gone from being the biggest employer in the US with over one million employees (going from memory) to less than 150,000 US employees today. GM is attempting to cut its way to prosperity. Maybe GM can finally compete with bold and innovative designs when they no longer have any employees. At this rate, it shouldn't be too much longer before we find out if that is the case. GM now complains healthcare costs account for $1500 per vehicle. Yet, if they would have maintained their market share, it would be $650 per vehicle. How much is it for Daimler or Honda? I don't know but it isn't zero whether it be the cost of national health care in Germany or Japan or healthcare costs for their US employees. Let's say it's $500. So, even with a $1000 higher cost per vehicle today, you mean to tell me GM can't differentiate their cars with innovative products are superior designs such that a consumer would be willing to pay $24,ooo for a breathtaking GM design versus $23,000 for a ho-hum competitive design? If so, GM needs a new marketing team. Well, the Wal-mart approach to marketing is another GM problem but I can only write about this topic for so long before I become infuriated. GM must be more aggressive with their designs and their entire turn around plan. GM must not be as good as the competition, they must be better or they will never get a satisfied Honda or Toyota customer to consider a GM product. The old saying goes that a lost customer or new customer takes ten times the effort to win over or win back than an existing customer. Do you think Honda and Toyota understand this? All too well.

The automobile industry isn't exactly known for its innovation. We still have transportation with four rubber tires, four doors and the same relatively crude drivetrain after one hundred years. Auto manufacturers are nearly impossible to kill off because they have historically been shielded from alot of competition. For most of GM's history, there were only a couple of companies which competed with it. So, GM shoved whatever kind of garbage out the door they saw fit. And, as a consumer with limited choices, you ate it or you didn't eat anything at all to a certain extent just like consumers in the Soviet Union. While barriers to entry are still high, that began to change significantly about thirty years ago. Now there are twenty major manufacturers vying for your spend and GM has lost market share nearly every year during that period of time. An unimaginable but true statistic. Unimaginable because if this happened in any other industry, GM would already have gone the way of the Dodo bird. ie, Extinct. If GM had the market share of thirty years ago, it would be a half a trillion dollar company and still the mightiest company on the planet. Instead, today, it is a declawed, whimpering shadow of its former self. Yet, inside of GM, the arrogance continued during this period of time. That arrogance has led to a crisis which will likely be resolved in only one outcome. Bankruptcy. Regardless of what GM does, because their mass has dimished into a smaller comparative company, they are now saddled with a disproportionate retiree burden which is likely unsolvable without a massive restructuring of those agreements. Did it need to be this way? Of course not. But it is and that is all that matters.

Let's look at automotive innovation. General Motors has spent more money on R&D in the last twenty years than America spent developing whole new technologies and whole new industries in the Apollo moon program. Much of everything you touch today was influenced by advances in the Apollo program. I can honestly say that was one government program that significant commercial benefits to American companies and consumers. So, America's entire investment for the Apollo program was approximately $100 billion. Last year GM spent $7 billion on research and development. So, for hundreds of billions in R&D we get cars with fuel efficiency 5-15mpg better than they were during the OPEC oil crisis of the 1970s. A 5.7 liter V8 truck gets a combined 14 miles per gallon today. In 1974 it was 10mpg. The Chevy Chevette got nearly 30mpg in 1975. Today, the Chevy Aveo gets a combined 30mpg. What gives? You mean to tell me $7 billion in R&D last year and GM cannot produce a car with better powertrain technology?

Let's be fair. Honda, BMW, Daimler, Toyota and others aren't much better. Cumulatively, the global auto companies have likely spent in excess of half a trillion dollars on R&D over the last few decades. Innovation and the automobile industry are pretty much mutually exclusive. Yes, engines burn cleaner. Yes, smaller engines develop more horsepower. Yes, we have better creature comforts. Yes, the quality has improved substantially. But real innovation, especially in power trains? Fuggedaboutit. So, why didn't GM or Toyota come up

with this twenty years ago? They will tell you it was because customers didn't want it. Or because there was no demand for it. We could argue till the cows come home but new industries, ideas and products are created daily which have no existing demand. Latent demand is everywhere. You don't know you need something until it is invented. Did you say you needed Google before its invention? A cell phone before it was invented? The auto industry is highly resistant to change and spends millions lobbying your government to make sure it stays that way.

Yet, we are likely to see a huge change in the automobile business. It will not be led by GM, Toyota or other traditional manufacturers. They will profit from it but the innovation leaders will be entrepreneurs, small flexible startups, innovation companies, university researchers and government led efforts at transformational change. I tend to think of it as a mini-revolution in transportation technology. It is not predicated on the high price of oil. I believe that is old news. The problem has been defined and that is the starting point for invention. The problem is energy independence so we don't have to spend $1 trillion on another Iraq War defending oil or $80 billion a year meddling in Middle East politics and, secondly, it is a new awareness our gluttony is destroying the planet and if we want a better place for our children we need to get our shit together as it pertains to waste, global warming and other ecological efforts. By the time it is all said and done, we may even be presented with many new transportation manufacturers. With advances in productivity, design capabilities, off the shelf componentry, virtual organizations and flexible manufacturing technology, it is conceivable boutique transportation manufacturers could be profitable with relatively low run rates. Today there is even a small American company which can retrofit a pickup to achieve 85 miles per hour top speed and 120 miles between charges using Lithium Ion battery technology. The recharge time? Ten minutes. Howsa about a recharging station? With technological advances such as this, that is not such a pipe dream. All of this is done with a vehicle cost of $40,000. How low could that price be driven in volume by Toyota or GM? Why is this important? Our electricity can be derived from clean coal technologies, natural gas and nuclear power which does not come from unstable regions. ie, Electricity powered or assisted cars can help achieve energy independence and may help reduce emissions. Battery and energy storage technology is making rapid advances as are many other options now that we have clearly defined our mission.

What must GM do to be successful in its turnaround efforts? Well, more than I care to type but here are a few major areas GM must focus on.

1.) GM has lost entire generations of customers. Those customers may never come back. GM needs to focus on the genXers as Toyota and Honda focused on the baby boomers. Studies have shown young kids have a positive opinion of GM. Yet, what do they offer that a genXer wants? A Suburban? A Cadillac DeVille? Does GM even know who its customers are? Anyone who pays Tiger Woods big bucks to be a spokesman for Buick, a car purchased by 70 year old men, doesn't get it. Do you think Tiger Woods drives a

Buick Rendezvous? I don't care if Buick drivers play golf. GenXer Tiger Woods fans or yuppie Tiger Woods fans don't drive Buicks. Bold

Cadillac V-Series or trimmed out Escalades? Yes. Buick? NO. Tiger Woods would drive a 500 horsepower Escalade or V-Series. And, just as his arrangement with TAG Heuer, Tiger Woods could be a boon to GM if used properly.

2) GM needs bold and innovative designs. Robert Lutz was brought in as Vice Chair to get GM back on track with bold and successful designs. To date Lutz has failed. Not because his designs are not significantly improved but because they are too staid. There are signs of life with the Solstice, Aura, Cadillacs and coming pickups but the majority of GM designs aren't even best in class let alone good enough to maintain market share.

3) GM needs to upgrade its interiors. GM interiors are the worst in the business. Some of the new designs are drastically better but they simply are not competitive with best in class as of yet except for the Cadillacs.

4) GM needs to build better relationships with its suppliers. GM has abused suppliers so long that in times such as today, suppliers are not willing to extend GM much leniency. Purchasing in the auto industry is by far the biggest expense and cost controls are extremely important but GM working as a partner with suppliers as opposed to an adversary will yield long term benefits for both. Partnering, GM actually has the ability to think more strategically with a partner and, if necessary, help their suppliers improve their efficiencies through common business processes, integrated design methodologies and shared technological/productivity advances.

5) GM must find every possible means to cut costs, conserve cash and share common platforms globally. Today, GM simply does not have the cash to spend on new development that some of the more healthy competitors have. This may actually act to quicken the demise of GM if they cannot keep their designs new and fresh while others are able.

6) GM needs to find a way to use their global design and engineering centers of excellence more effectively. Today GM is building small car expertise in one region, pickups in another and midrange offerings in another as examples. Instead GM needs to find a way to have Asian, European and American engineering teams working effectively un unison on the same design. A twenty four hour cycle of development. ie, Should development work be done on a next generation product in the US, it will be done in eight hour days. Should engineering be shared by a global team, work could be done in Asia, then as the sun sets, work is started in Europe then the US. Development is done on a 24 hour a day basis which speeds innovation and drives the competitive advantage few other car companies have.

7) GM needs to rebuild faith in its brand within the US. Whether this is done with extended warranties, by improved dealer experiences, a transformation of how it services customers or by direct marketing is irrelevant. GM needs an all encompassing full court press on the American consumer and it should start now.

8) GM should be the innovation leader in next generation transportation technology. GM is a powerhouse of technology, creativity and brain power that simply needs unleashing. GM is surely capable of driving new technology into the market place before anyone else. Whether that be hybrids, clean diesel technology, safety, the driver experience or efficiency. Innovation in itself would do much to transform GM's brand images.

9) GM must develop a culture of risk taking, responsibility and empowerment. GM has "big company disease". A common ailment that is usually rectified by active boards or shareholders or competition which forces change. A company in such a staid industry has been able to survive for forty years with no focus and nearly total apathy. GM is internally focused, has no idea who its customers are and has no sense of urgency. It uses its heft to maintain its existence rather than innovation, quality or breathtaking designs. That is why, forty years later, companies such as Nissan, Honda and Toyota now rival GM in global scale and size. They, on the other hand, have been consumer focused and maniacal about winning in the market.

10) GM must define its brands and who its customers are. I look at some of these products rolling out of GM and wonder who are they targeting. First off, no one in their 20s. Most in their 50s, 60s or even 70s. After dominating the luxury segment, GM has all but forfeited that arena to a dozen manufacturers. What are my choices if I'm 35, single, well heeled and want a sporty car? A Grand Prix? A Buick Lucerne? A Chevy Malibu? Huh? What if I'm 25 and want something that is a reflection of my youthful independence or individuality? My point is that GM has not had a cohesive brand management strategy in forty years.

There is much more GM needs to do but the customer experience is the most important focus for GM. Whether that is pre-sale, post-sale or as part of ownership experience. And so is innovation. GM must be viewed as the innovation leader. With all of the intellectual capital within GM, that would not be a problem with the right leadership team.

It has yet to be determined whether GM has reached the threshold of pain necessary for its revival but if this is not the time it soon will come. One thing I am certain of. When the pain is severe enough, GM will finally emerge as a formidable foe. Ford as well. Crisis creates opportunity and brings about change which otherwise is not possible. As difficult as it may be to fathom, GM will once again drive fear into all those who dare to cross paths with The General. The only question is if Rick Wagoner or another will be the one able to deliver the goods.

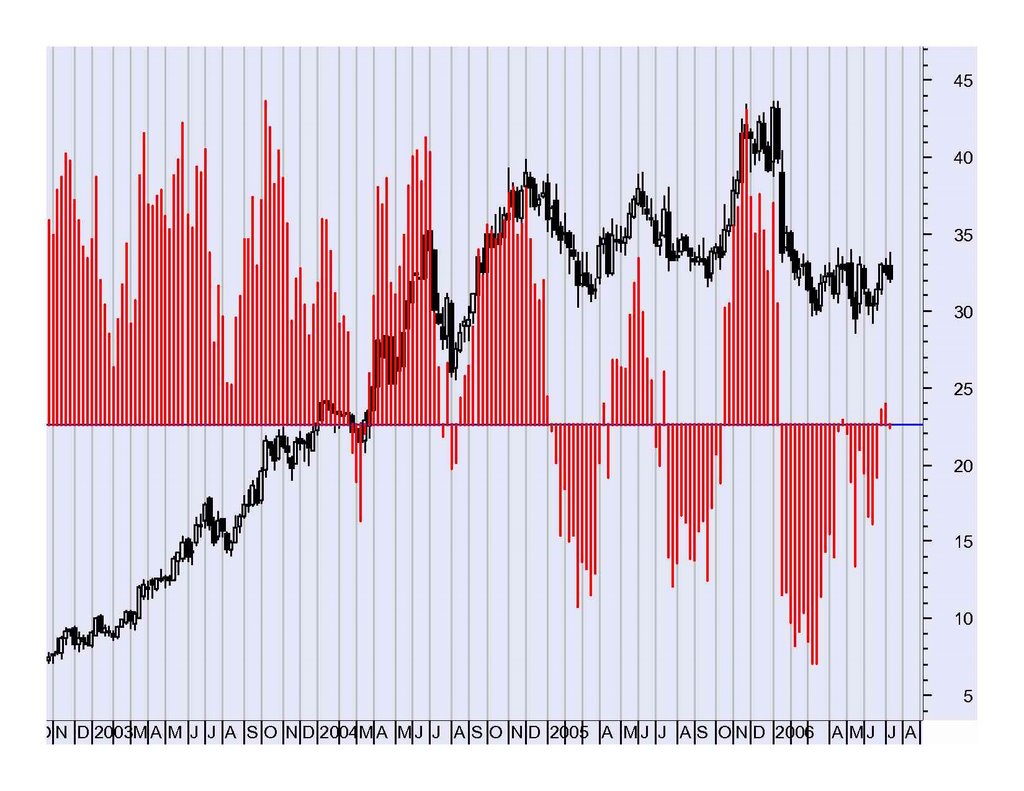

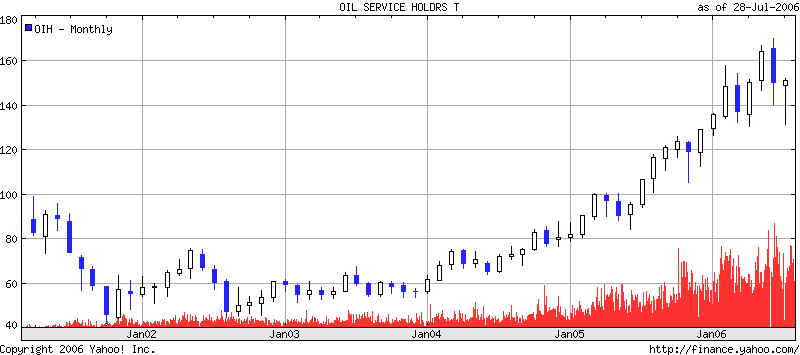

Above is the Oil Service Sector ETF, OIH. I put this chart up for a specific reason. Jeff Saut, whom I view as one of the most trustworthy and savvy public figures on Wall Street has just been quoted on Bloomberg as still being an energy bull. Clicking on his name will take you to his regular commentary which I read when I get the chance. While I believe oil will eventually drop significantly or collapse, its appeal will likely not tarnish overnight. So, $10 oil isn't just around the corner. It might actually take years to collapse. But the oil stocks are a different story. So, what do you see on this chart? Anything unusual? Anything foreboding? Remember, patterns repeat. Patterns can be in equity markets or outcomes to certain economic cycles or your own behavior. Very few of us break the cycle of patterns in our own life so why would human behavior ever change? We use the past to divine the future because human behavior is the one constant in an ever changing world.

Above is the Oil Service Sector ETF, OIH. I put this chart up for a specific reason. Jeff Saut, whom I view as one of the most trustworthy and savvy public figures on Wall Street has just been quoted on Bloomberg as still being an energy bull. Clicking on his name will take you to his regular commentary which I read when I get the chance. While I believe oil will eventually drop significantly or collapse, its appeal will likely not tarnish overnight. So, $10 oil isn't just around the corner. It might actually take years to collapse. But the oil stocks are a different story. So, what do you see on this chart? Anything unusual? Anything foreboding? Remember, patterns repeat. Patterns can be in equity markets or outcomes to certain economic cycles or your own behavior. Very few of us break the cycle of patterns in our own life so why would human behavior ever change? We use the past to divine the future because human behavior is the one constant in an ever changing world.