Are Large Caps Cheap?

It seems everywhere I look, people are now jumping on the large cap bandwagon. Sure, large cap is cheap compared to parts of the market which are ridiculously valued. But, it appears people never learn. Large cap is not cheap. Nor are the market leaders over this rally, large cap technology, defensive.

I'm going to use a stock I absolutely abhor as an example: IBM. Remember, I'm talking about the stock as an investment not the company. IBM is the perfect Dow study given its in the technology business which is a highly cyclical industry.

It's hard not to find someone who isn't bullish on IBM. The Motley Fool has IBM picked as a top stock for 2007. Although, I can state that their reasons for doing so show a fundamental lack of understanding of the IT and business consulting space. None of the reasons they state have any merit except for a strong patent engine. Yet, I discount patents for two reasons. First, IBM has always been a patent machine yet the stock has underperformed for forty years. Secondly, I am very aware of the abused patent process and how companies like IBM, HP, Microsoft and others take advantage of the system. They'd patent a new method to tie shoes if they could and many patents aren't much more compelling. ie, The patent system is in need of updating. Motley Fool also picks IBM as a winner using an extremely loose and unsophisticated discounted cash flow analysis. On an unrelated topic, if this is how one determines value based on discounted cash flows, I'd rather take my chances playing the lottery.

It isn't just the Motley Fool I'm picking on. It's S&P, nearly all of the analysts following IBM which rate it a buy and any number of Wall Street personalities. The arguments I hear most often are a low PE and it is a mega cap which will hold up comparatively well if the market weakens. Well, I guess if one finds a 62% drop in IBM from 2000-2002 palatable compared to a 38% decline for the Dow, then one might conclude it will hold up comparatively in any decline.

Now, let's take a look at reality. Using dividends and price-to-book, IBM is the 4th and 11th most expensive stock in the Dow with a 1.3% yield and trading at over 4x book value. That is not cheap for a mega cap. Especially a mega cap with single digit top line growth expectations. Another fact. IBM has been dead money for nearly a decade. The $70-90 price range we seem stuck in was first reached in 1998. In fact, if you take away 1996-1998, IBM has pretty much flat lined for forty years. Additionally, technology profits are extremely cyclical and a PE of 16 could easily double with a weak economy. ie, IBM could easily be trading at a PE of 25 or 30 should we see an earnings recession or worse. Now, in a raging bull market that isn't a primary concern but will we remain in a raging bull market? The market is strong right now but remember the market was strong right up until the May sell off too. We are in a period of elevated risk to say the least. Should we see a reversion to the mean and single digit PEs on S&P 500 stocks before we get out of this cyclical funk, IBM will likely experience a severe haircut. 1-2x book would not unreasonable for a reasonably mature company seeing single digit long term growth prospects. While most people would absolutely laugh at the prospect, there is a reasonable technical argument that IBM could retest the high $20s with a severe recession. I'm not saying that will happen but that is a valuation consistent with levels seen in the 1970s. That's a far cry from the $200+ fair value cited at the Motley Fool.

In order to be a successful investor, one must be disciplined. In order to determine if an investment is "cheap", one should aspire to use successfully proven techniques such as the work pioneered by Benjamin Graham and followed by Warren Buffett not the generalized drivel coming from anyone who can get their face in front of a camera. I find it more comforting to know my views are consistent with those of Richard Russell, Walter Deemer, John Templeton, Warren Buffett and other old timers rather than many of my generation who believe Wall Street is a slot machine.

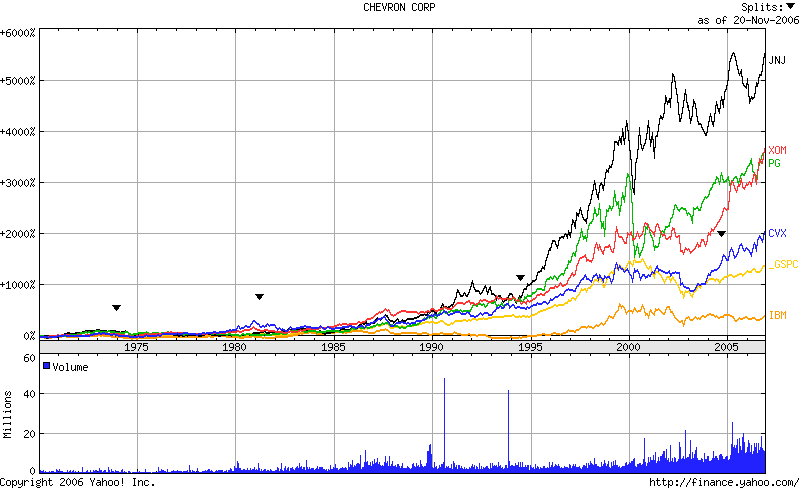

Were I a buy & hold investor, the last thing I would own is technology unless we were in a very long wave secular bull market. Below is a relative performance chart of Chevron, Johnson & Johnson, Exxon Mobil, Procter & Gamble, IBM and the S&P 500 over the last forty years. IBM hasn't even come close to returns half as good as the S&P 500 let alone the dull businesses of those drilling oil and making soap. Is there some compelling reason why history is not going to repeat itself? Maybe the new PowerPC chip in the Playstation 3? That's a joke for those who tout this as a reason to own IBM.

Now, let's look at IBM over the past two years. Has it made a 2 year high? No. Does it look like it is going to? No. To the contrary, as I pointed out with half a dozen stocks popping major gaps a month or so ago, IBM being one of them, the stock has done nothing since popping that gap. In fact, as of this week, the stock has a negative return over the last month. It appears IBM is turning lower. Temporary? Maybe but I doubt it. Each time buying pressure has reached this level of overbought over the last seven years, IBM has shown considerable weakness. Cheap? Not even close. Empower yourself. Do your own homework if you choose to own individual stocks.

Finally, let's look at a longer term chart of IBM. An absolutely ugly chart might I add. Each time IBM has reached the lower trend line, it has rallied for more than a decade. Will we see a continuation of that fact? Many other stocks have already broken their long term bull market trend lines. It looks like IBM is biding time. Similarly, other Dow components and large cap technology stocks show a comparable mid-term pattern as I discussed with Wal-mart some months ago. Is large cap cheap? Well, if I was forced to buy something right now, it would be large cap stocks. But it isn't cheap in my world and buying a mature, slow growth company with a 1.3% dividend yield is no different than pulling the slot machine at the Bellagio.

I'm going to use a stock I absolutely abhor as an example: IBM. Remember, I'm talking about the stock as an investment not the company. IBM is the perfect Dow study given its in the technology business which is a highly cyclical industry.

It's hard not to find someone who isn't bullish on IBM. The Motley Fool has IBM picked as a top stock for 2007. Although, I can state that their reasons for doing so show a fundamental lack of understanding of the IT and business consulting space. None of the reasons they state have any merit except for a strong patent engine. Yet, I discount patents for two reasons. First, IBM has always been a patent machine yet the stock has underperformed for forty years. Secondly, I am very aware of the abused patent process and how companies like IBM, HP, Microsoft and others take advantage of the system. They'd patent a new method to tie shoes if they could and many patents aren't much more compelling. ie, The patent system is in need of updating. Motley Fool also picks IBM as a winner using an extremely loose and unsophisticated discounted cash flow analysis. On an unrelated topic, if this is how one determines value based on discounted cash flows, I'd rather take my chances playing the lottery.

It isn't just the Motley Fool I'm picking on. It's S&P, nearly all of the analysts following IBM which rate it a buy and any number of Wall Street personalities. The arguments I hear most often are a low PE and it is a mega cap which will hold up comparatively well if the market weakens. Well, I guess if one finds a 62% drop in IBM from 2000-2002 palatable compared to a 38% decline for the Dow, then one might conclude it will hold up comparatively in any decline.

Now, let's take a look at reality. Using dividends and price-to-book, IBM is the 4th and 11th most expensive stock in the Dow with a 1.3% yield and trading at over 4x book value. That is not cheap for a mega cap. Especially a mega cap with single digit top line growth expectations. Another fact. IBM has been dead money for nearly a decade. The $70-90 price range we seem stuck in was first reached in 1998. In fact, if you take away 1996-1998, IBM has pretty much flat lined for forty years. Additionally, technology profits are extremely cyclical and a PE of 16 could easily double with a weak economy. ie, IBM could easily be trading at a PE of 25 or 30 should we see an earnings recession or worse. Now, in a raging bull market that isn't a primary concern but will we remain in a raging bull market? The market is strong right now but remember the market was strong right up until the May sell off too. We are in a period of elevated risk to say the least. Should we see a reversion to the mean and single digit PEs on S&P 500 stocks before we get out of this cyclical funk, IBM will likely experience a severe haircut. 1-2x book would not unreasonable for a reasonably mature company seeing single digit long term growth prospects. While most people would absolutely laugh at the prospect, there is a reasonable technical argument that IBM could retest the high $20s with a severe recession. I'm not saying that will happen but that is a valuation consistent with levels seen in the 1970s. That's a far cry from the $200+ fair value cited at the Motley Fool.

In order to be a successful investor, one must be disciplined. In order to determine if an investment is "cheap", one should aspire to use successfully proven techniques such as the work pioneered by Benjamin Graham and followed by Warren Buffett not the generalized drivel coming from anyone who can get their face in front of a camera. I find it more comforting to know my views are consistent with those of Richard Russell, Walter Deemer, John Templeton, Warren Buffett and other old timers rather than many of my generation who believe Wall Street is a slot machine.

Were I a buy & hold investor, the last thing I would own is technology unless we were in a very long wave secular bull market. Below is a relative performance chart of Chevron, Johnson & Johnson, Exxon Mobil, Procter & Gamble, IBM and the S&P 500 over the last forty years. IBM hasn't even come close to returns half as good as the S&P 500 let alone the dull businesses of those drilling oil and making soap. Is there some compelling reason why history is not going to repeat itself? Maybe the new PowerPC chip in the Playstation 3? That's a joke for those who tout this as a reason to own IBM.

Now, let's look at IBM over the past two years. Has it made a 2 year high? No. Does it look like it is going to? No. To the contrary, as I pointed out with half a dozen stocks popping major gaps a month or so ago, IBM being one of them, the stock has done nothing since popping that gap. In fact, as of this week, the stock has a negative return over the last month. It appears IBM is turning lower. Temporary? Maybe but I doubt it. Each time buying pressure has reached this level of overbought over the last seven years, IBM has shown considerable weakness. Cheap? Not even close. Empower yourself. Do your own homework if you choose to own individual stocks.

Finally, let's look at a longer term chart of IBM. An absolutely ugly chart might I add. Each time IBM has reached the lower trend line, it has rallied for more than a decade. Will we see a continuation of that fact? Many other stocks have already broken their long term bull market trend lines. It looks like IBM is biding time. Similarly, other Dow components and large cap technology stocks show a comparable mid-term pattern as I discussed with Wal-mart some months ago. Is large cap cheap? Well, if I was forced to buy something right now, it would be large cap stocks. But it isn't cheap in my world and buying a mature, slow growth company with a 1.3% dividend yield is no different than pulling the slot machine at the Bellagio.

<< Home