Let's Look At The Bull Case

I'm a firm believer in maintaining an open mind regarding the future. Not just today but always. Most readers might be surprised to know that am uber bullish on the long term. That is a statement regarding global economies but most specifically the US, Britain & Canada. I make that conclusion based on the data in the pipeline I see building as I type this. It just so happens I am quite concerned in the short term. When the ship rights itself and how the short term plays out is the question.

The future is not an absolute. It is measured in probabilities which are constantly changing. If you find your views very black and white versus shades of grey, your thought processes might be too rigid. One should be able to articulate a positive and a not so positive future if you are going to be a successful investor. It is an easy exercise and one I believe everyone should develop not just for investing but for life's experiences. Many times I'll take the opposite side of an argument just to see if the other person actually knows what they claim to know. If for no other reason, you can learn to hone your hypothesis or rigorously defend it.

You don't want to be so married to a potential outcome that when markets start a major assault higher, you may sit back and wait. And wait. And wait. Similarly in the opposite direction, being so bullish that you refuse to acknowledge pitfalls like 2000, 2001 and 2002. In 2003, many were very bearish and they waited and waited. From trough to peak, the semiconductor index was up 120% that year. The Nasdaq nearly 100%. It was one of the best investment years in modern times and many missed it. Similarly, in 2005, many were very bearish. The oil service sector, as an example, was up nearly 100% that year. It's one thing to expect negative patterns to develop, but as long as the market is assaulting new highs, you should never fight the tape.

While the current state of "stuff" leads me to believe a stock market correction is highly probable if not imminent, I also try to keep an open mind that the future might not turn out as expected. At some point you need to start allocating capital if your models turn positive or the markets make significant upside progress. I don't get too hung up on which way the market will go and you shouldn't either. You should be more concerned about educating yourself to ride either when we break out of this messy trading range. And we will. Today my long term model is in 100% cash and nothing has happened since May to change the behavior of that model. I choose to interpret my model as black or white. Cash or invested. But, I could just as easily define it as defensive and ride through the rough patches with defensive stocks. Yet, this cycle has typically punished even defensive stocks so I prefer a strategy of capital preservation. What does that mean about the future? Well, I can logically tell you how it will end but that may not come to pass. The probabilities are on my side as are some strong quantitative work but when I learn to read the tea leaves, I'll be sure to share it with all for the betterment of mankind.

So, let's review some key points of the bullish case. Maybe you have even more:

1) The economy is still relatively healthy and continues to grow albeit it is frazzled growth

2) Housing may not totally collapse or decline as precipitously as the worst case scenario anticipates

3) If we get wage inflation, and today we don't have it regardless of what is being reported, it will help prop up housing, retailing and other weak sectors

4) Historically, one sector has not been able to bring down the economy. Hence, housing alone is likely not going to crater the economy. Remember, housing sales are still at a brisk pace from a historical perspective regardless of the supply glut which could possibly be worked off with comparatively minor damage.

5) Large capitalization stocks are pretty cheap compared to any time in the last ten years.

6) Oil, commodity and energy prices seem to be abating as is inflation. That reduces a major burden on the consumer. To date, $300 million plus per day is staying in the consumer's pocket from the gasoline peak prices. That's a $120 billion per annum tax cut should it last.

7) Interest rates are still relatively low historically and the long end rates are getting lower thus adding support for the case of weak future inflation, support for housing and equities. Mind you, rates are not that low from a historical perspective. They are close to average in historical terms.

8) Global wealth will continue to create demand for American goods

9) There is still way too much money in the system and that will prop up asset prices

10) American stocks have underperformed and outperformance is now a reasonable hypothesis after six years of a near death experience.

11) The markets have discounted alot of negative news

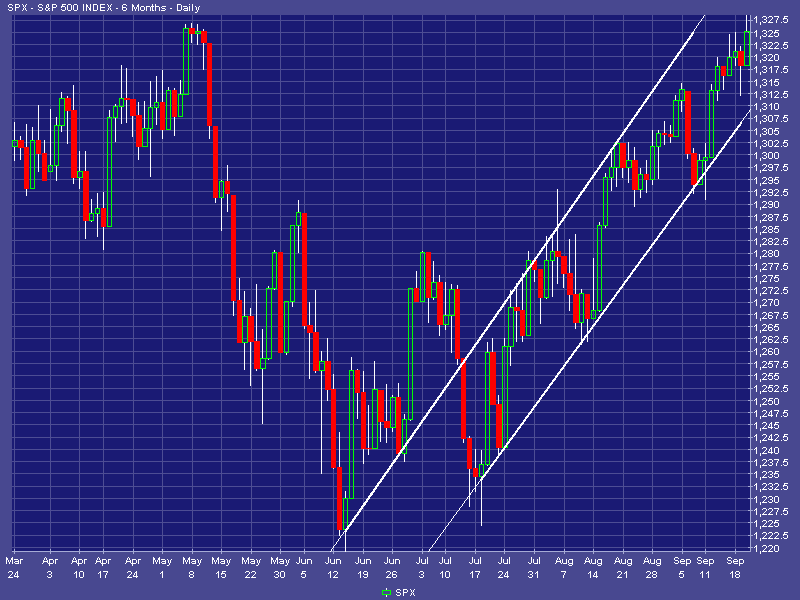

As I've stated a couple of times before, the market's decline from May onward was not sustainable. Just when certain groups had totally cratered, the perma-bears could see the whites of the bull's eyes. The mood was intensely negative and the bears could clearly visualize the kill. The world was over. The problem was just about when they could actually see it, the market quit going down and some stocks went up quite a bit. Oops, sorry but no bull dinner yet for the bears. At the rate of decline we were experiencing, the world would have come to an end and market would have been to zero by the end of the year. Fortunately, that didn't happen because I'm not ready to meet my maker.

If we get monthly declines on average of 2-3% a month, we will likely see an overall decline of what I think is possible by October of 2007. This isn't a generally accepted thesis for those expecting a rapid collapse but let's see what happens. This is a framework I can live with. A fluid attempt at rationality based on historical and mathematical predictions as is used by the Fed or others attempting to predict the future. Models change over time as should your thinking processes as you digest additional data points. If we are free and clear by October of 2007, our chances of an imminent decline have diminished significantly from where we sit today. That said, don't count on it.

Moral of the story? Perma-bears and perma-bulls are always losers in the long run because they are rigid thinkers wedded to an outcome and belief which is clearly well outside of the normal distribution of events. Example? Thousands in every aspect of life. There is one such person I am reminded of today by reading a regular commentary from a well respected investment advisor. That example is a New York City economist with a very active subscription based web site. He has repeatedly called for the end of the world since 2004. Three years later and he's still wrong. And his subscribers paid for what? Bad advice and poor investing returns. That's why opinions are a nice read but one needs to listen to what the markets are telling you when it comes to investing. This same economist would have likely missed a 500% rally during the Great Depression as well. Why? Because the economy was awful yet the stock market blew through the roof. I could dig a 500% rally from here. But, again, don't count on it.

If you don't already, you should plan to gain input from multiple sources including many who don't agree with your view. Remember, two things. First, psychologically you give more credence to people who agree with your methods of reasoning whether your reasoning is right or wrong. Second, your brain is conditioned to be significantly more sensitive to negative news. Studies have shown that you need 2-3x as much positive feedback just to balance the negative feedback. This served us well as cavemen and allowed Elmer Fuddstone to defeat the sabre-toothed rabbit but it serves you poorly in the investing world.

All of that said, don't become a perma-bull just because the thirty stocks leading the S&P and Dow are flirting with new highs. But, can you envision an economy six to twelve months from now which is recovering? If so, don't be so wedded to the bear argument because the market will move up on such an outcome and it will do it today not nine months from now.

The future is not an absolute. It is measured in probabilities which are constantly changing. If you find your views very black and white versus shades of grey, your thought processes might be too rigid. One should be able to articulate a positive and a not so positive future if you are going to be a successful investor. It is an easy exercise and one I believe everyone should develop not just for investing but for life's experiences. Many times I'll take the opposite side of an argument just to see if the other person actually knows what they claim to know. If for no other reason, you can learn to hone your hypothesis or rigorously defend it.

You don't want to be so married to a potential outcome that when markets start a major assault higher, you may sit back and wait. And wait. And wait. Similarly in the opposite direction, being so bullish that you refuse to acknowledge pitfalls like 2000, 2001 and 2002. In 2003, many were very bearish and they waited and waited. From trough to peak, the semiconductor index was up 120% that year. The Nasdaq nearly 100%. It was one of the best investment years in modern times and many missed it. Similarly, in 2005, many were very bearish. The oil service sector, as an example, was up nearly 100% that year. It's one thing to expect negative patterns to develop, but as long as the market is assaulting new highs, you should never fight the tape.

While the current state of "stuff" leads me to believe a stock market correction is highly probable if not imminent, I also try to keep an open mind that the future might not turn out as expected. At some point you need to start allocating capital if your models turn positive or the markets make significant upside progress. I don't get too hung up on which way the market will go and you shouldn't either. You should be more concerned about educating yourself to ride either when we break out of this messy trading range. And we will. Today my long term model is in 100% cash and nothing has happened since May to change the behavior of that model. I choose to interpret my model as black or white. Cash or invested. But, I could just as easily define it as defensive and ride through the rough patches with defensive stocks. Yet, this cycle has typically punished even defensive stocks so I prefer a strategy of capital preservation. What does that mean about the future? Well, I can logically tell you how it will end but that may not come to pass. The probabilities are on my side as are some strong quantitative work but when I learn to read the tea leaves, I'll be sure to share it with all for the betterment of mankind.

So, let's review some key points of the bullish case. Maybe you have even more:

1) The economy is still relatively healthy and continues to grow albeit it is frazzled growth

2) Housing may not totally collapse or decline as precipitously as the worst case scenario anticipates

3) If we get wage inflation, and today we don't have it regardless of what is being reported, it will help prop up housing, retailing and other weak sectors

4) Historically, one sector has not been able to bring down the economy. Hence, housing alone is likely not going to crater the economy. Remember, housing sales are still at a brisk pace from a historical perspective regardless of the supply glut which could possibly be worked off with comparatively minor damage.

5) Large capitalization stocks are pretty cheap compared to any time in the last ten years.

6) Oil, commodity and energy prices seem to be abating as is inflation. That reduces a major burden on the consumer. To date, $300 million plus per day is staying in the consumer's pocket from the gasoline peak prices. That's a $120 billion per annum tax cut should it last.

7) Interest rates are still relatively low historically and the long end rates are getting lower thus adding support for the case of weak future inflation, support for housing and equities. Mind you, rates are not that low from a historical perspective. They are close to average in historical terms.

8) Global wealth will continue to create demand for American goods

9) There is still way too much money in the system and that will prop up asset prices

10) American stocks have underperformed and outperformance is now a reasonable hypothesis after six years of a near death experience.

11) The markets have discounted alot of negative news

As I've stated a couple of times before, the market's decline from May onward was not sustainable. Just when certain groups had totally cratered, the perma-bears could see the whites of the bull's eyes. The mood was intensely negative and the bears could clearly visualize the kill. The world was over. The problem was just about when they could actually see it, the market quit going down and some stocks went up quite a bit. Oops, sorry but no bull dinner yet for the bears. At the rate of decline we were experiencing, the world would have come to an end and market would have been to zero by the end of the year. Fortunately, that didn't happen because I'm not ready to meet my maker.

If we get monthly declines on average of 2-3% a month, we will likely see an overall decline of what I think is possible by October of 2007. This isn't a generally accepted thesis for those expecting a rapid collapse but let's see what happens. This is a framework I can live with. A fluid attempt at rationality based on historical and mathematical predictions as is used by the Fed or others attempting to predict the future. Models change over time as should your thinking processes as you digest additional data points. If we are free and clear by October of 2007, our chances of an imminent decline have diminished significantly from where we sit today. That said, don't count on it.

Moral of the story? Perma-bears and perma-bulls are always losers in the long run because they are rigid thinkers wedded to an outcome and belief which is clearly well outside of the normal distribution of events. Example? Thousands in every aspect of life. There is one such person I am reminded of today by reading a regular commentary from a well respected investment advisor. That example is a New York City economist with a very active subscription based web site. He has repeatedly called for the end of the world since 2004. Three years later and he's still wrong. And his subscribers paid for what? Bad advice and poor investing returns. That's why opinions are a nice read but one needs to listen to what the markets are telling you when it comes to investing. This same economist would have likely missed a 500% rally during the Great Depression as well. Why? Because the economy was awful yet the stock market blew through the roof. I could dig a 500% rally from here. But, again, don't count on it.

If you don't already, you should plan to gain input from multiple sources including many who don't agree with your view. Remember, two things. First, psychologically you give more credence to people who agree with your methods of reasoning whether your reasoning is right or wrong. Second, your brain is conditioned to be significantly more sensitive to negative news. Studies have shown that you need 2-3x as much positive feedback just to balance the negative feedback. This served us well as cavemen and allowed Elmer Fuddstone to defeat the sabre-toothed rabbit but it serves you poorly in the investing world.

All of that said, don't become a perma-bull just because the thirty stocks leading the S&P and Dow are flirting with new highs. But, can you envision an economy six to twelve months from now which is recovering? If so, don't be so wedded to the bear argument because the market will move up on such an outcome and it will do it today not nine months from now.