It's Vacation Time

I will be on vacation for the next nine days so there will be no posts during that time. Happy holidays to all.

Our goal is to provide reasoned, relevant and often contrarian commentary on topics of international investing, global economic developments and business strategy in a format that is easy to understand and thought provoking.

Support this site with a donation.

Terms of Use & Disclaimer: First off, I don't take anything on here too seriously and you shouldn't either. These are simply sardonic rantings of Bill, my alter ego, often meant to agitate for peaceful & nonviolent reform. This web site reflects the views of its authors. It is unaffiliated with any NASD broker/dealer. Statements on this site do not represent the views or policies of anyone other than its authors. The information on this site is provided for discussion purposes, comedic relief and entertainment only and are not investing recommendations. The authors may have positions in securities mentioned herein. Under no circumstances does this information represent a recommendation to buy or sell securities. While information discussed on this site was gathered from what are believed to be reliable sources, in no way is informational accuracy guaranteed. All information on this site may contain errors and omissions. Trading and investing involves high levels of risk. Always consult a licensed financial advisor or broker before making any and all investment decisions. Authors of this site and any sites which are fed by said site, including Open Salon and others, will assume no responsibility for the actions of the reader and user. Readers and users agree, as condition to accessing this site, to release and hold harmless this site's authors from all liability in connection with this site or any views posted on this site. All readers and users of this site agree that use of this site requires acceptance to the current Terms Of Use & Disclaimer and that current terms include any and all use and material from site inception. If you do not understand these statements in their entirety or do not agree to be bound by this current agreement, you must immediately discontinue use of this site. This Terms Of Use & Disclaimer may change at any time and it is the reader's and user's responsibility to review, understand and abide by any updates.

QUOTES FOR DAILY REFLECTION, SELF-IMPROVEMENT AND SUCCESS

"Sometimes it falls upon a generation to be great. You can be that great generation." - Nelson Mandela

"A leader is best when people barely know he exits. When his work is done, his aim fulfilled, they will say, 'We did it ourselves.'." - Lao Tzu

"Do not fear to be eccentric in opinion, for every opinion now accepted was once eccentric." - Bertrand Russell

"Courage is the power to let go of the familiar." - Raymond Lindquist

"My religion is very simple. My religion is kindness." - Dalai Lama

"Hard work has made it easy. That is my secret. That is why I win." - Nadia Comaneci

"Dream no small dreams for they have no power to move the hearts of men." - JW von Goethe

"There are no secrets to success. It is the result of preparation, hard work and learning from failure." - Colin L. Powell

"The fishermen know that the sea is dangerous and the storm terrible, but they have never found these dangers sufficient reason for remaining ashore." - Vincent van Gogh

"Success is not final. Failure is not fatal. It is the courage to continue that counts." - Winston Churchill

"Kindness can become its own motive. We are made kind by being kind." -Eric Hoffer

"Until he extends the circle of his compassion to all living things, man will not himself find peace." -Albert Schweitzer

"In the fields of observation, chance favors only the prepared mind." -Louis Pasteur

"Ours is a world of nuclear giants and ethical infants. We know more about war than we know about peace, more about killing than we know about living." -Omar Bradley

ANCIENT PROVERBS

"Fall seven times; stand up eight."

"He who asks a question is a fool for a minute; he who does not remains a fool forever."

"A single conversation across a table with a wise man is worth a month's study of books."

YOU CAN BE THAT GREAT GENERATION. DO SOMETHING GREAT TODAY BY SUPPORTING A CHILD IN NEED:

Add the TimingLogic feed to your reader using the feed icon below

Click here to receive free TimingLogic updates by email subscription

I'm an electrical engineer and mathematician by training. My career has spanned diverse areas of expertise from being part of a team which designed the world's most powerful computers to corporate consulting around business transformation and information-based solutions to being a corporate sales and marketing executive in the information technology and business consulting space. I’ve led teams responsible for innovative and transformative solutions and been part of teams that helped set strategy for many of America's greatest companies. Two of my interests are econometrics and quantitative - qualitative analysis. Over the years I have developed risk-based models and trading systems meant to identify significant investment opportunities and periods of extreme risk. My blog is an outlet for another of my passions, writing. I generally consider myself a contrarian. Therefore, many of my rantings are meant to encourage people to question what they believe to be true.

First off, I have to say that I try to practice the mindset that I am neither bullish nor bearish on stocks or the economy. ie, I am open to change and not tied to a particular point of view. Those who point to massive debt or point to overspending by consumers as a reason to think stocks are going down simply to not have historical precedence on their side. Some of the biggest moves in the stock market have been when America had massive debt burdens. Much higher as a percent of GDP than today. The likely reasoning behind that fact is the worst may be behind us at those moments. People see accumulated trends, either positive or negative, and believe they will continue forever and they never do. Another data point is the stock market had a 400% rally in the Great Depression. So, today, just as people label Americans as spendaholics, we are most likely to become a nation of savers over the coming years. That may start out as a trend of spending less rather than sticking money in our mattresses starting tomorrow.

Are the markets cheap? I guess that depends on perspective. Are they cheap compared to six years ago? Yes? Compared to ten years ago? Maybe. Compared to fifteen years ago? Not as. Compared to the last one hundred years. Nope. The problem is that people develop these mindsets over periods of economic prosperity that are simply not sustainable. The trend never lasts forever. But, people say there is so much liquidity today or so much money chasing stocks or the world is a different place than fifty years ago. Maybe. But, do you realize that fifty years ago they were saying the same thing? That was their golden age of technology, economic growth, great wealth and enlightenment. One constant is human behavior. That never changes. And neither does the attempted rationalization as to why things are different this time. That is why the stock market never changes.

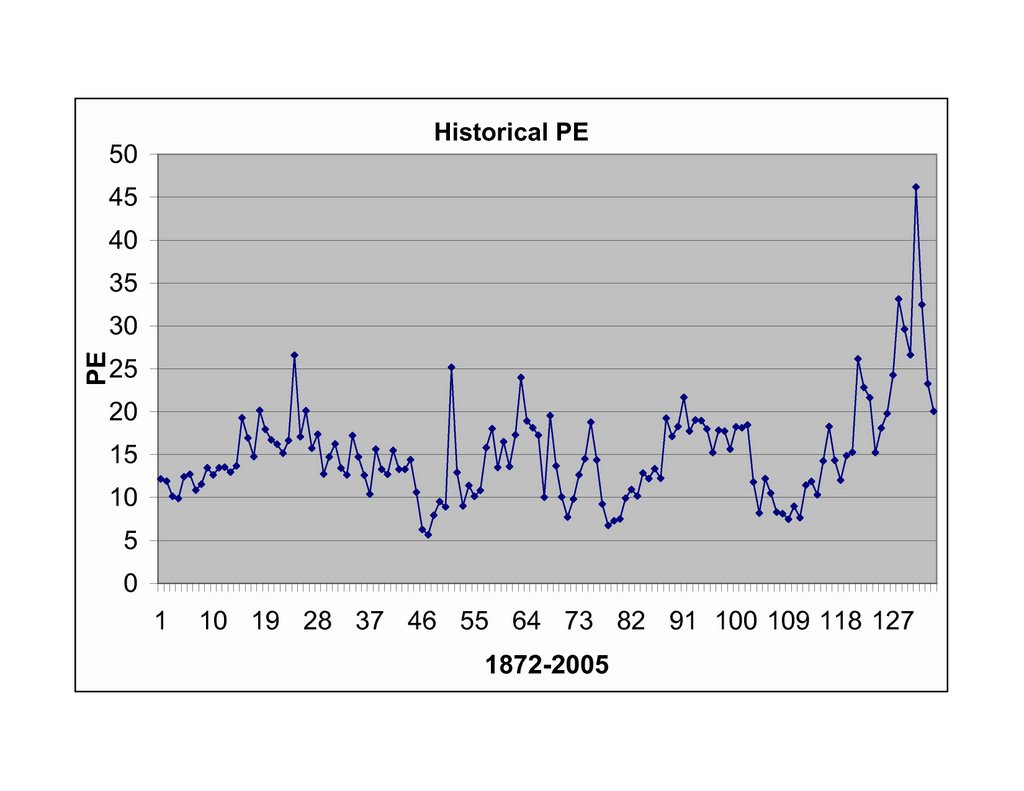

So, in the last four years, what has happened to the stock market PE ratio? It has contracted. Not only here but in nearly every major stock market around the world. When Wall Street is bullish about the future of the economy, stock market PEs around the globe expand along with earnings. The rationale for this is that people are much more confident about the future and are willing to pay a higher multiple for stocks so PE's expand along with earnings. This time earnings have expanded but PE ratios have contracted. Historically, this is a very ominous sign for stocks. It means investors are not confident about the future so they are willing to pay less for a stock.

So, is this cycle of growth in stock prices sustainable? Is the market cheap? Well, earnings are the most cyclical in the last fifty years. Now, what does that mean? That many of the company earnings propping up the stock market are highly cyclical or in simple english, their earnings are like a yo-yo. They go up alot then come down alot. Hence cyclical. So, now that they have gone up alot, what have they done historically? You may fill in the blank yourself.

So, if earnings start to decline, will the PE ratio be 38 on the Russell 2000 or 17 on the S&P 500? No, the PE will rise as earnings fall. Historically, whenever earnings fall and PEs rise because of that, stocks fall because they are overvalued. So, is the market cheap? Compared to 2000, it's very cheap. What's the old saying? Those who don't heed history are doomed to repeat it?

We can't get any follow through in stocks. We are at levels of oversold which should eventually drive a rally of some sorts. But, unless the bulls get it in gear soon, we are going lower.

So, anyone take a look at the program trading volume on the NYSE? 73%? Uh, is that like some kind of record? Ok, so there may be some double counts in there. When was the last time we saw this? Can you say 1987? And the macroeconomic circumstances could be loosely interpreted as similar as well. Forget about what "kind" of growing economy we had, more along the lines of international trade, the dollar, gold, real estate bubbles overseas, etc.

This is NOT a healthy correction that we see in bull markets as we are led to believe by many. But bear markets always start with the bulls calling this an expected correction. The reality is this is a rout in developing markets and a market where growth in tech equity prices peaked two years ago.

Who's pushing the trigger on that rout? Seems to me we had this kind of scenario once before where a handful of financial institutions controlled most of the trading on Wall Street but now it's globally. When was that? Oh, yea. 1929. Didn't Congress fix that situation? Why they sure did. It was called Glass-Steagall. And, what happened to that reform? In the hey day of Pax Americana and goldilocks the greedy bastards on Wall Street lined your politicians pockets and they blew it up. Obviously for the betterment of Ma and Pa America.

http://www.pbs.org/wgbh/pages/frontline/

shows/wallstreet/weill/demise.html

So, does the concept of reversion to the mean apply to more than just equity markets? We are told by many that it is a natural progression that we move away from heavy industries into finance and services. A service based economy. ie, We are too sophisticated to be bothered with menial labor. We outsource that to the developing world. Maybe. Finance is a higher percentage of

So, is housing a bubble? Maybe not. But, for forty years housing tracked about one to one with new household creation. Now, it's about two and one half to one. And mortgages? Well, the mortgages as a percentage of total banking loan revenue has doubled in the last few years to anything well beyond its modern historical averages. So, now those same financial institutions that control your equity markets are also overexposed to risk in real estate. Can you say banking crisis? I don't think it will happen but risks are rising and we are creating a potential mess at some point with lax regulatory controls. And why do we have those lax controls? Greed. Only the kind available to American financial institutions that donated hundreds of millions to our very willing elected representatives that would get the laws overturned for favors. Monetary favors. In the end, will the entire process lead to self destruction? ie, Will Wall Street’s drive for more and more power ultimately lead to its own self destruction and rebuilding? Like 1929 when the head of the NYSE was carted off to jail?

So, are we in the heavily regulated 1970s where inflation was the problem or are we in the wild and wooly 1920s where regulation was yet to be adopted to keep Wall Street from hosing us all? Don't just think in terms of

Anyone who thinks the markets are selling off because Bernanke is mealy mouthed about inflation is one of the three monkeys: see, hear or speak no evil. The imbalances caused by thirty years of deregulation and bubbles are what concerns the global markets. It’s the precarious nature of stable instability. In the US,

Unless otherwise indicated, the written and graphic material on this site is the copyrighted intellectual property of "the company", LLC (the actual company name is withheld for privacy purposes. Contact the site owner for the actual company name.) and may not be reproduced without written permission. Copyright 2006-2017, "The Company", LLC. Unauthorized reproduction of this material is prohibited, protected under copyright laws and defended by "The Company", LLC. For educational purposes the material on this site may be linked to other websites. Fair use notice: This site may make use of copyrighted material, the use of which has not always been specifically authorized by the copyright owner. Use for purposes such as criticism, comment, news reporting, teaching, scholarship, or research is not an infringement of the 1976 Copyright Act and is considered “fair use” of any such copyrighted material as provided for in section 107 of the US Copyright Law. In accordance with Title 17 U.S.C. Section 107, the material on this site is distributed without fee or payment of any kind to those who have expressed a prior interest in receiving the included information for research and educational purposes. If you wish to use copyrighted material from this site for purposes that go beyond “fair use”, you must obtain permission from the copyright owner. These terms may change at any time and it is the responsibility of the reader to review, understand and abide by any updated terms.

Today, as we speak, many market pundits are calling the bottom here. HaysMarketFocus.com has posted on their site as of June 14th the following:

I Believe!!

The Environment is Finally—after 6 months—Setting Up for Healthy Bull

6/14/06

Now I have tremendous respect for Don Hays but as I recall seeing him on TV, he is a "long" only investor and not a market timer, per se. So, that means he is invested at all times including the massacre from 2000-2003 and should we ever repeat the 1930s or anything similar, he would again remain invested. I simply to not believe in that philosophy. How does one know when markets are coming back up? We lost nearly $13 trillion in global equity markets in the fall from 2000. That is why market timing is a key competency one should look for in my opinion. Ask the Japanese about the Nikkei. Down for 17 years just as they were christened the heir apparent to America's economic mantle. Don is not the only well respected advisor who has called a bottom here. So has Barry Ritholtz. Another very pragmatic advisor whom I have the utmost respect for. The good news is both trade with their recommendations so Barry in particular will get out with minimal damage if his call is wrong. And don't be terribly concerned if a call is wrong. Most will be right. I relate to Barry's style. And, while no one likes to lose money, would you rather lose 2% on a short term loss or ride the markets down for an 80% loss as in 2000? Just a possible scenario not a prediction.

Me? Well, my models are built to make money. In both rising and falling markets. And they've been refined with gut wretching losses. We may yet be near a bottom but my models are not giving me a buy. And, while there is no such thing as 100%, since 2000, they have picked off every major bottom as a great time to buy. That is the problem with anticipation. No one wants to miss a great rally because we are oversold. But, the problem is you can stay oversold for a long time. It is something we are not used to given the bull market of the 1990s is all most people know.

So, let's wait and see how this market shakes out before we jump back in. Maybe it will be this week. Maybe it will be next month.